SDMI INDEX METHODOLOGY

SDMI – INDEX PHILOSOPHY

The SummerHaven Dynamic Metals Index (“SDMI”) was developed by SummerHaven Index Management to provide an active metals index benchmark for commodity investors. The SDMI is based on the notion that commodities with low inventories will tend to outperform commodities with high inventories, and that priced-based measures, such as futures basis and price momentum, can be used to help assess the current state of commodity inventories1.

SDMI – INDEX CONSTRUCTION

The SDMI consists of 10 metals contracts – six industrial metals and four precious metals – that are included in the index each month. Five metals are selected each month through the steps outlined below, which are designed to identify metals in a low inventory state. The metals selected will be weighted more heavily than their respective base weights, and the remaining five metals not selected will be weighted less heavily than their respective base weights during any given month.

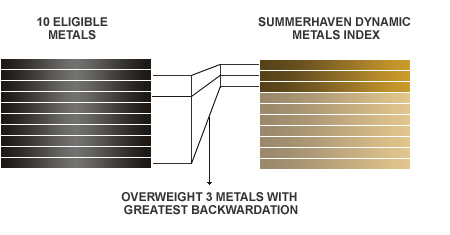

STEP 1: Commodity Selection – Backwardation

Choose 3 metals with the greatest backwardation (or least contango). Backwardation is measured as the annualized % price difference between the futures price for the closest-to-expiration contract and the next closest-to-expiration contract for each commodity.

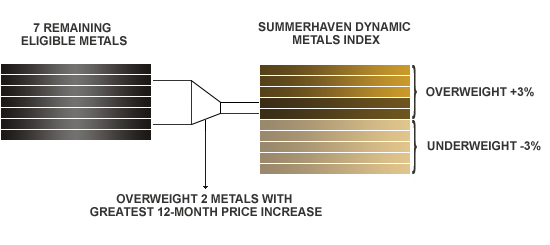

STEP 2: Commodity Selection – Momentum

From the remaining 7 metals, choose 2 commodities with greatest 12-month price momentum. Momentum is measured as the % price difference between the futures price for the closest-to-expiration contract and the price of the closest-to-expiration contract 12-months ago for each commodity.

The 5 metals selected will have their weighting for the following month increased by 3%. The 5 metals not selected will have their weighting for the following month decreased by 3%. Base weights for each of the 10 eligible metals is detailed in the table below:

| ELIGIBLE METALS | BASE WEIGHTING |

| Aluminum | 15.00% |

| Copper | 19.00% |

| Lead | 4.00% |

| Nickel | 10.00% |

| Tin | 4.00% |

| Zinc | 10.00% |

| Gold | 15.00% |

| Silver | 15.00% |

| Platinum | 4.00% |

| Palladium | 4.00% |

STEP 3: Contract Month Selection

For each of the 10 index commodities, SDMI selects the contract month with the greatest backwardation (or least contango), taking into account the allowed contracts and maximum tenor for each commodity market.

The maximum eligible tenor is measured as the number of months starting from the maturity of the closest-to-expiration contract. The previous not withstanding, the contract expiration is not changed for that month if a commodity remains in the index, as long as the contract does not enter expiry or enter its notice period in the subsequent month.

| COMMODITY SYMBOL | COMMODITY NAME | ALLOWED CONTRACTS | MAX. TENOR |

| LA | Aluminum | All 12 calendar months | 12 |

| HG | Copper | All 12 calendar months | 12 |

| LL | Lead | All 12 calendar months | 7 |

| LN | Nickel | All 12 calendar months | 7 |

| LT | Tin | All 12 calendar months | 7 |

| LX | Zinc | All 12 calendar months | 7 |

| GC | Gold | Feb, April, June, Aug, Oct, Dec | 12 |

| SI | Silver | Mar, May, Jul, Sep, Dec | 5 |

| PL | Platinum | Jan, Apr, Jul, Oct | 5 |

| PA | Palladium | Mar, Jun, Sep, Dec | 5 |

SDMI Rebalancing:

Price observations for the steps described above are taken on the fifth-to-last business day of each month. SDMI rebalancing takes place during the last four business days of the month (the “Selection Date”). At the end of each of these days one fourth of the prior month portfolio positions are replaced by the new over-weighted or under-weightedposition in the commodity contracts determined on the Selection Date.

| REBALANCING START | REBALANCING END |

| Thursday, January 26, 2017 | Tuesday, January 31, 2017 |

| Thursday, February 23, 2017 | Tuesday, February 28, 2017 |

| Tuesday, March 28, 2017 | Friday, March 31, 2017 |

| Tuesday, April 25, 2017 | Friday, April 28, 2017 |

| Thursday, May 25, 2017 | Wednesday, May 31, 2017 |

| Tuesday, June 27, 2017 | Friday, June 30, 2017 |

| Wednesday, July 26, 2017 | Monday, July 31, 2017 |

| Monday, August 28, 2017 | Thursday, August 31, 2017 |

| Tuesday, September 26, 2017 | Friday, September 29, 2017 |

| Thursday, October 26, 2017 | Tuesday, October 31, 2017 |

| Monday, November 27, 2017 | Thursday, November 30, 2017 |

| Tuesday, December 26, 2017 | Friday, December 29, 2017 |

« Back

1 Geert Rouwenhorst, SummerHaven partner and Yale professor, is a recognized leader for his academic research linking commodity futures returns to inventories:

See “The Fundamentals of Commodity Futures Returns” under Reference Materials.